What You Will Pay For AI

Or how high will the frontier lab vig go?

The Switch

On June 3, Lindy founder Flo Crivello announced that he had switched 100 percent of the company’s traffic from Anthropic to the open weights Chinese model DeepSeek v4. The change, he wrote, would save Lindy “millions of $” while increasing performance across many of its core use cases. This was not a benchmark prediction or a complaint about an expensive invoice. It was a customer taking its entire workload elsewhere.

The obvious story is that competition has arrived. Open source (actually open weights…), and primarily Chinese open source models, are finding homes in startups and Fortune 500 companies. Cloudflare serves Zhipu AI’s GLM 5.2 model natively in its Workers AI service, as does Microsoft.

The $10 trillion question is what happens to the frontier labs now. Is their reign of terror at an end? Having spent billions on models that the Chinese distill for millions, will they go quietly into that good night, tail between their legs, to the ignominy of bankruptcy and burst bubble, as our friend Michael Burry (of The Big Short) expects?

Clearing Capability The Threshold

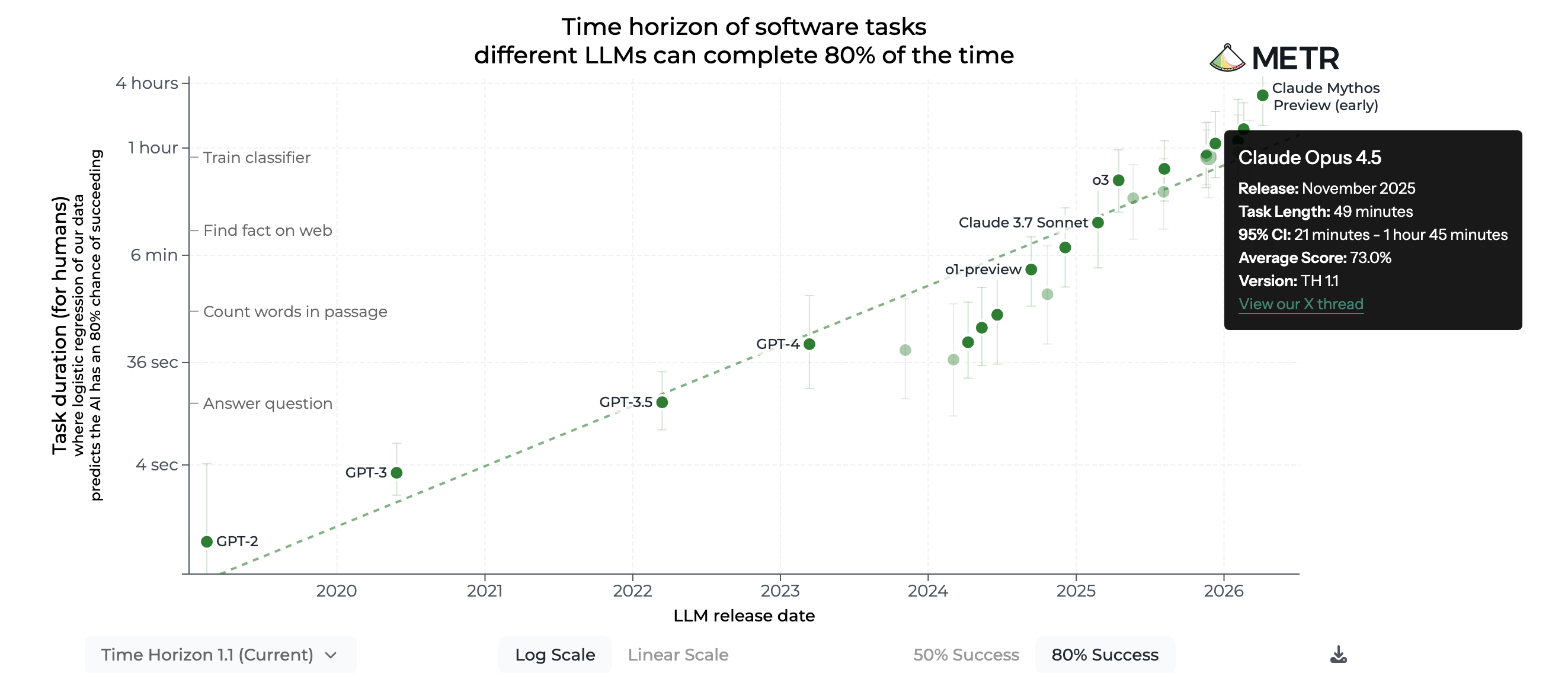

To understand how Anthropic could become one of the fastest-growing companies in history and then lose Lindy’s entire workload on price and performance, rewind seven months.

On November 24, 2025, Anthropic released Claude Opus 4.5. METR - an organization that evaluates the ability of AI agents to complete increasingly long tasks - estimated that Opus 4.5 could complete software tasks requiring approximately 49 minutes of human work with 80 percent reliability. Its predecessor, Opus 4.1, had reached only 23 minutes.

That may sound like an incremental improvement. Economically, it was not.

The important event was not that the model gained another 26 minutes. It was that it crossed a threshold. Below that threshold, an engineer could ask the model to write code, but still had to supervise it, recover from failures, and repeatedly redirect it. Above it, the model could complete a growing class of bounded tasks from beginning to end.

With the right scaffolding - tool access, tests, context management, retry loops and what came to be called harness engineering - the model could begin to work through software problems using some of the same collaborative machinery human engineers had built for one another.

The market response was extraordinary. Anthropic ended 2025 at roughly $9 billion in annualized revenue. By May 2026, the company said its run rate had crossed $47 billion. That increase cannot be attributed to a single benchmark result or model release. But it is consistent with a broader change: AI had moved from helping engineers compose code to completing valuable units of engineering work.

Software developers began to see the writing on the wall. Their occupation was not about to disappear, but its internal division of labor was being rewritten.

That was the beginning of the 2026 coding-agent boom.

Tier 1: I Just Want It Done

Software engineering was an ideal first market for capable AI because many coding tasks are unusually specifiable and verifiable. In test-driven development, the tests can be written before the code. The machine can run those tests repeatedly and receive an immediate signal about whether its work succeeded.

Bounded software tasks are therefore unusually clean examples of Tier 1:

A Tier 1 task is an existing production activity for which AI creates value primarily by changing the cost, speed, scale, capacity, consistency, or quality of producing an already-valued output or service, rather than by changing the buyer’s position relative to rivals or creating a new source of demand.

The economic value of a Tier 1 task is anchored to the economics of the production process it replaces:

Willingness To Pay₁ ≈ expected cost savings + expected additional earnings − adoption and risk costs

Once Opus 4.5 could complete an hour-sized unit of engineering work with adequate reliability, Anthropic was no longer selling merely an interesting model. It was selling substitutes for some of the most expensive labor inputs in the economy.

That explains the revenue explosion.

It also explains Lindy’s departure.

Once DeepSeek could produce the same output at lower cost, Flo Crivello, the founder of Lindy, became unwilling to pay Claude’s vig.

This cost comparison is likely to occur for all Tier 1 tasks, which compose the bulk of operations at every company.

The defining characteristics of Tier 1 tasks:

The activity, need, or economic objective already exists and is recognized.

A baseline worker, process, vendor, or technology performs the same economic function.

The buyer would still value the result if no strategic rival existed.

The principal gain is improved cost, speed, scale, capacity, consistency, or quality.

AI changes production of an existing output or service rather than principally creating a new market.

Demand does not depend primarily on beating a rival or creating a new market.

Errors, supervision, integration, and verification are economically material costs.

The work may be one-off, open-ended, creative, subjective, contextual, or judgment-heavy.

Examples of Tier 1 activities include

transcription

bookkeeping

document extraction

code generation

customer support

translation

compliance review

research synthesis

design review

medical diagnosis

marketing copy produced for an existing product.

This brings us to the next major category of tasks.

Tier 2: I Need It More Than You

On April 7, 2026, Anthropic announced Claude Mythos Preview. The model was supposedly an extremely strong cybersecurity researcher, which posed so much danger to existing systems that instead of releasing Mythos to the public, Anthropic instead released it to members of Project Glasswing, a consortium of the largest datacenter operators and software firms. Nicholas Carlini, the most cited cybersecurity researcher in history and Anthropic’s security lead, said “the nice balance we had between attackers and defenders in the last 20 years or so seems like it is probably coming to an end”.

Cybersecurity, and indeed all adversarial games which yield a winner and a loser, are examples of Tier 2 activities.

A Tier 2 task changes the buyer’s expected payoff by improving or defending the buyer’s position relative to other actors competing for scarce rents, market share, opportunities, attention, status, or strategic advantage.

The economic value of a Tier 2 activity is simply the value of not losing.

Willingness To Pay₂ ≈ increase in probability of winning x value of rents + expected value of avoiding loss − adoption and risk costs

The defining characteristics of Tier 2 tasks:

Participants compete for an existing scarce prize: customers, market share, attention, capital, contracts, talent, political power, or economic rents.

The buyer’s value depends materially on performance relative to rivals, not merely on meeting an absolute standard.

Competitors’ capabilities, adoption decisions, and responses enter directly into the value of the task.

Early adoption can create an offensive advantage; later adoption may become necessary simply to preserve competitive parity.

The value of an advantage depends on its scarcity and usually declines as the capability diffuses.

Willingness to pay reflects the expected improvement in winning probability, market share, bargaining power, or avoided competitive loss.

Competitive responses can produce an arms race in which every participant spends more without proportionately increasing total social output.

Private returns may substantially exceed social returns when AI primarily redistributes existing rents rather than creating new surplus.

Tier 2 need not be strictly zero-sum: the activity may also improve productivity or consumer welfare, but its dominant source of private value is positional.

The work may be routine or creative, objective or subjective, simple or technically difficult. Those properties do not determine the tier.

Examples of Tier 2 activities

Sales prospecting and targeting: Identifying and converting valuable customers before rivals do.

Algorithmic trading: Acting on information or price discrepancies before other market participants.

Dynamic pricing: Improving margins by predicting demand and competitors’ pricing responses.

Competitive bidding: Optimizing bids for contracts, acquisitions, advertising inventory, or spectrum.

Litigation strategy: Increasing the probability of winning a case or obtaining a favorable settlement.

Political campaigning: Winning votes, donations, endorsements, or scarce public attention.

Talent acquisition: Identifying and recruiting high-value workers before competing employers.

Cybersecurity: Defending against adaptive attackers or discovering vulnerabilities before adversaries exploit them.

Military and intelligence analysis: Securing an informational or operational advantage over adversaries.

Sports strategy: Improving the probability of victory against adapting opponents.

Platform recommendation systems: Capturing user attention and engagement from competing platforms.

Reputation and influence management: Improving a person’s or organization’s relative standing within a contested field.

Looking at the list of Tier 2 activities gives one pause. These are complex tasks that require careful consideration of large amounts of data, judgement calls, historical context and expertise. The tasks are usually performed by highly qualified and trained professionals, often holding MBAs, JDs or PhDs.

Success is also unverifiable before the fact. Whether you gain an advantage over your opponent is evident only in the arena.

Have the frontier labs proven they can deliver on Tier 2 capability? The jury is still out, but the organizations which live in Tier 2 are not waiting to find out:

Commands around the world, including the US Central Command in the Middle East, use Anthropic’s Claude AI tool, people familiar with the matter confirmed

In the hyper competitive world of financial trading, market making firm Citadel, with Assets Under Management of $570 billion.

And for us at Citadel, that has allowed us to unleash a much broader array of use cases for AI. And it has been really interesting to watch, to be blunt, work that we would usually do with people with masters and PhDs in finance over the course of weeks or months being done by AI agents over the course of hours or days.

These are not these are not mid-tier white collar jobs. These are like extraordinarily high skilled jobs being, I’m going to pick a word, automated by agentic AI. And I gotta tell you, I went home one Friday actually fairly depressed by this because you could just see how this was going to have such a dramatic impact on society.

Tier 2 activities are fundamentally competing for a share of existing rents. If the frontier labs are able to prove that using their AI models confers a clear advantage for even a short time, they will have found the thing every vendor dreams of and almost none achieve: a product whose price does not fall when the technology improves (as long as the frontier lab stays ahead).

And while advantage is unverifiable in advance, its absence will be verified in the arena, at full cost. The demand is insurance shaped: you pay the labs so you will not lose because you don’t have the best AI.

Which brings us to the actual frontier:

Tier 3: What We Don’t Know Whether AI Can Do

This is really where the inhabitants of the AI bubble diverge from the rest of the world. Bubble-dwellers believe that AI will do things that it has never before done. The rest of the world, especially investors like Michael Burry, regard this belief with scorn. And indeed, it seems more an article of faith rather than scientific fact. The extrapolation of nonsense variables into the stratosphere seems designed to dumbfound rubes, and throughout the whole cacophony, the whispers of “this time it is different” inflame rational investors with disgust.

A Tier 3 task searches for or realizes a materially new product, platform, production method, scientific capability, business model, or category of demand whose economic value cannot be adequately inferred from the price of an existing task or from a fixed contest over existing rents.

AI has produced Tier 3 capability before, with Alphafold in Dec 2020, which won Demis Hassabis and John Jumper of Google Deepmind their Nobel Prize, and arguably with self-driving in recent years, with both Waymo and Tesla making progress using different approaches. Both of these advances required enormous amounts of specialized data, and produced models which were only good for their one particular task.

Language models however, are expected to gain generality. As Łukasz Kaiser, a co-author of the landmark “Attention is All You Need” paper says:

But in our heads, we have a lot of different worlds and these are all represented in text mostly. So I think the language models have already a model of like all of our abstract worlds.

The first signs that the frontier language models are acquiring Tier 3 capability has come from the field of mathematics, which has tasks which are both verifiable (like coding) but also have never been accomplished before (unlike software engineering).

On May 20, 2026, OpenAI reported that a frontier AI language model had disproved the unit distance conjecture, an open problem in mathematics for over 80 years, and notably, one that every mathematician in the field had studied and failed to solve.

This has been one of Erdős’ favorite problems, I have heard him myself mentioning the problem multiple times in his lectures. I believe it would be fair to say that every mathematician working in Combinatorial Geometry thought about this problem, and lots of mathematicians working in other areas spent at least some time thinking about it… The solution of the problem by the internal model of Open AI is, in my opinion, an outstanding achievement, settling a long-standing open problem. The fact that the correct answer is not n1+o(1)n 1+o(1) is surprising, and the construction and its analysis apply fairly sophisticated tools from algebraic number theory in an elegant and clever way.”

Disproving the unit distance conjecture does not have economic value of course, but people in AI expect much much more, and soon. OpenAI’s Alexander Wei, who was on the reasoning team that developed the model in question:

More Erdos problems have continued to be solved since that initial announcement, and non Erdos problems have begun falling as well.

The expectation of some AI researchers, especially employees of Anthropic and OpenAI, is that this process of producing landmark scientific research has a) kicked off and b) some of the research will in turn accelerate AI development.

If it does happen, it really would be transformative, and likely within a short period of time.

Defining characteristics of Tier 3:

The commercially valuable output may not be fully specifiable in advance.

No stable market price exists for the final result before the market is formed.

Search and learning are part of the task, not merely costs incurred before execution.

Uncertainty may be Knightian: probabilities, outcome categories, and demand are themselves unclear.

Technical invention alone is insufficient; adoption, distribution, institutions, complements, and behavior determine economic success.

Returns are strongly skewed: many experiments fail and a small number produce very large gains.

Private appropriable value may be far below total social value because of knowledge spillovers and consumer surplus.

A successful Tier 3 innovation can generate many later Tier 1 production tasks and Tier 2 competitive contests.

Classification is probabilistic ex ante and more reliable ex post.

Examples of Tier 3 :

Developing AlphaFold: Creating a new scientific capability for predicting protein structures at scale, accelerating biological research and expanding the set of tractable drug-discovery problems.

Developing fully self-driving vehicles: Creating a new transportation capability that could enable autonomous mobility services, reorganize logistics and urban infrastructure, and generate markets that cannot exist when every vehicle requires a human driver.

Creating the iPhone and App Store: Establishing a mobile-computing platform and an ecosystem of businesses that previously could not exist in that form.

Discovering CRISPR-based gene editing: Creating a new technological capability with applications across medicine, agriculture, and biological research.

Inventing the transistor: Expanding the feasible set of electronic products and enabling entirely new industries.

Developing a commercially viable fusion reactor: Creating a new source of energy production rather than operating existing generation more efficiently.

Inventing a new battery chemistry: Making previously infeasible forms of transportation or energy storage economical.

Creating the modern search-engine advertising market: Establishing a new mechanism for matching commercial demand with user intent.

Developing reusable orbital rockets: Discontinuously changing launch economics and enabling new space-based markets.

Discovering a new material: Producing properties that enable products or production methods that were previously infeasible.

Creating Artificial General Intelligence

Many of mankind’s riskiest and highest valued endeavors are the results of successful completion of Tier 3 tasks or projects. Because failure is normal, we have typically funded portfolios of basic science through governments and nonprofits, and commercially promising experiments through venture capital and corporate R&D.

The portfolio cannot be valued by averaging the projects. Most may fail. One extreme winner may determine the return:

Willingness To Pay₃ = increase in (probability-adjusted winners + option value + portfolio spillovers) − follow-on capital − expected losses − search and experimentation costs.

The formula looks precise. The inputs are not. In Tier 3, you may not know the probability of success, the possible outcome categories, the future demand or even the right business model.

The Problem Of Uncertain Outcomes

And so we come to crux of the issue.

Tier 1

Tier 1 tasks have known payoffs. With a known ROI (Return on Investment), CFOs of Fortune 500 companies could make commitments to Claude Code, with confidence, in the last 7 months.

The market understands Tier 1. There is growing realization that much of enterprise software is in Tier 1, and this has begun to scare software vendors.

Let us not bring that dynamic into the AI era, with a small number of AI systems capturing all the economic returns, while entire industries find their knowledge commoditized right out from underneath them.

However it is also true that open source models have begun to contest the Tier 1 revenue pool. The frontier labs still have the more efficient models, and make greater margin from the same amount of compute due to this, but contested margins are capped margins.

Tier 2

Tier 2 users are competitors for a revenue pool who must decide whether winning requires the services of a frontier AI. If it does, these users become permanent rent payors to the frontier model firms, as long as the models they create outperform competing models.

The market has not yet understood Tier 2. A frontier model firm cannot be supplanted by an open source model offering lower prices without equivalent or better performance. The frontier model firms will successfully establish themselves as permanent rent collectors in every vertical where competition matters.

Tier 3

The frontier labs have not yet fully proven that they have Tier 3 capabilities that matter economically yet. They are however, already experimenting with methods to monetize Tier 3 capability.

OpenAI CFO Sarah Friar sketched a future in which the company’s business models evolve beyond subscriptions and could include royalty streams tied to customer results.

Speaking on a recent podcast, Friar floated the possibility of “licensing models” in which OpenAI would get paid when a customer’s AI-enabled work produces measurable outcomes.

In one example, she pointed to drug discovery: if a pharma partner used OpenAI technology to help develop a breakthrough medicine, the startup could take a licensed portion of the drug’s sales. The pitch, she suggested, is alignment: OpenAI would make money when its customers do.

- BusinessInsider - Jan 21, 2026

The initial experiments were through partnerships.

Eli Lilly - OpenAI - Jan 2024 - Collaboration to discover novel antimicrobials for drug-resistant bacteria

Eli Lilly - Google Isomorphic Labs - Jan 2024 - Multi-target research collaboration to discover small molecule therapeutics

However, the problem the frontier labs face is that

pharma companies regard target generation as at most 10% of the work of bringing a drug to market. The firms have too many targets to test as it is, and the bulk of the work is in the phased clinical trials the drug must go through in order to prove safety and efficacy.

the pharma companies are unable to evaluate the increase in success probability that is conferred by using the frontier lab model.

The labs meanwhile believe their technology is considerably more valuable than what the market is currently willing to pay for Tier 3 capabilities. In fact, Alex Karp, Palantir’s CEO, asked this very question

If it was so valuable, let’s say I can make you $1 billion tomorrow, wouldn’t I say I’ll make you $1 billion and I want 30%. Why are they charging for tokens if its so valuable?

This gap, what I call the commercialization gap, is the key problem that the frontier labs must solve in order to meet their capital expenditure commitments in the years ahead.

Commercialization Gap: The gap between what frontier AI is capable of creating and what customers can presently recognize, value, organize around, and pay for.

Which brings us to the end game:

Unless the market is willing to pay what it takes to support the capex the frontier labs need for Tier 3 capability, the labs will have to directly commercialize the technologies they develop. They would have no choice but to enter the near term addressable markets in competition with some of their customers.

This may look like direct entry like Anthropic announced in June 2026, spin-offs like Isomorphic from Google, or lab leaders departing from the mothership and being seed funded by lab employees, like Liam Fedus of OpenAI founding Periodic Labs to do material science.

The labs may also start to restrict access to their technology for competitive rather than safety purposes, as is suspected of Anthropic.

Implications

What are the key implications of the task taxonomy outlined above?

1. There is no single market price for intelligence

The same model may generate a customer-support response, advise on a billion-dollar acquisition and discover a commercially valuable molecule. The tokens may cost the same to produce, but the economic value of the outputs differs by orders of magnitude.

Model pricing based purely on compute is therefore unlikely to survive. The current model categories and reasoning settings are likely to be internalized by the frontier labs at some point in order to perform model routing internally. The long-run question is how much of the value created the model provider can capture.

2. Tier 1 margins will be utility like

Tier 1 can produce enormous productivity gains without producing durable profits for frontier labs. Once several models can perform the same task adequately, customers will route the work to the cheapest acceptable supplier.

The result may resemble cloud infrastructure: rising consumption, falling unit prices somewhat shielded by customer lock-in and brand, but in constant competition with large field of other vendors.

3. For enterprises: your AI procurement should be a tier audit.

The single most expensive mistake of the next five years will be paying Tier 2 prices for Tier 1 tasks — frontier tokens for bookkeeping — or its mirror, running Tier 2 contests on commodity models to save money (bringing DeepSeek to a Citadel fight). Rule of thumb: if the ROI calculation contains a competitor’s name, it’s Tier 2; pay up. If it contains a wage rate, it’s Tier 1; negotiate down.

4. Tier 2 is where frontier labs may obtain their strongest near-term pricing power

A customer engaged in litigation, cybersecurity, trading or military planning cannot safely choose a cheaper model merely because it is almost as good. A small capability difference may change the outcome of a very large contest.

But the lab is not necessarily a permanent rent collector. Its pricing power lasts only while its advantage remains scarce, credible and economically consequential.

5. AI policy should distinguish creation from redistribution

Tier 1 primarily raises productivity. Tier 2 may produce useful improvements, but it can also intensify rent-seeking and arms races. Tier 3 can create enormous growth and spillovers, yet private investors may underfund it because they cannot capture all the resulting value.

A sensible policy regime would not treat these activities identically. It might promote diffusion in Tier 1, scrutinize arms races and concentration in Tier 2, and support experimentation and knowledge spillovers in Tier 3.

6. The commercialization gap will push frontier labs into their customers’ industries

If a model can create a billion-dollar drug but pharmaceutical companies will pay only for tokens or target generation, the lab has an incentive to develop the drug itself.

Frontier labs may consequently become venture studios, pharmaceutical developers, cybersecurity companies, defense contractors and financial institutions—not because vertical integration was their original plan, but because direct participation may be the only way to capture Tier 3 value.

7. The commercialization gap sets the capex clock — it's a race between two dates.

Direct commercialization is slow (FSD took fifteen years; drugs take a decade of trials) while capex commitments compound now. So the real question is whether Tier 2 annuity revenue can bridge the interval between "capability exists" and "capability monetizes through owned ventures." This reframes lab finances entirely: Tier 1 revenue proves scale, Tier 2 revenue is the bridge loan, and Tier 3 is the balloon payment. A lab that loses the frontier loses Tier 2 rents and therefore loses the ability to wait for Tier 3 — which is why the frontier race is existential.

8. Verification is the binding constraint, so Tier 3 arrives domain-by-domain in verification order.

Math came first because proofs are checkable. The sequence follows verifiability, not value: math → code/algorithms → simulable physics and chip design → materials (fast synthesis loops) → biology (slow, regulated trials) → business-model innovation (no verification exists at all). Implication: the highest-value Tier 3 domains (drugs, AGI-driven new industries) monetize last, and the interim revenue comes from unglamorous verifiable niches. Corollary: anyone building verification infrastructure — autonomous labs, high-throughput synthesis, clinical-trial acceleration, formal verification — is selling the bottleneck, the picks-and-shovels of Tier 3.

9. Buy Tier 1 task-by-task, Tier 2 contest-by-contest, Tier 3 option-by-option

The C-suite should re-audit its AI portfolio quarterly - not because the economic tiers automatically change, but because capabilities diffuse, competitors respond and new production possibilities appear.

For every important workflow, executives should ask:

Is this production, competition or creation?

What is the cheapest model that can perform it?

Does frontier capability materially change the result?

If the project succeeds, would it create a new market or production possibility?

Who owns the harness, data and evaluations?

Who owns any resulting intellectual property?

Can the provider use what it learns to compete with us?

How quickly will today’s frontier advantage diffuse?

And thats the kicker

Ask not merely what the token costs. Ask what the token can do for you

The market’s current debate is dominated by Tier 1: frontier-scarce capabilities becoming commodities. In six months, bounded coding tasks went from barely commercially feasible for frontier models to achievable by much cheaper open-weight alternatives.

But this is not evidence that the frontier labs have lost all pricing power. It means yesterday’s frontier has become today’s production input.

The labs have already migrated up. That is what Glasswing's 5x pricing was; that is what CENTCOM's deployment and Citadel's PhDs-in-hours are — the Tier 2 regime, arriving vertical by vertical, and the market has not yet recognized it. Tier 1 prices fall because someone else can do the task. Tier 2 prices hold because no one can afford to find out what the cheaper model costs them in the arena.

And beyond that, Tier 3 waits on the horizon — the promised land the frontier labs are actually navigating toward, the place where the technology stops substituting for existing work and starts creating products that have never existed. We may cross this year, or next, or in 2029 according to Ray Kurzweil, or 2035 according to Demis Hassabis — or never, according to Michael Burry.

Here is what should give the skeptics pause. Tier 1 has a price, and it is falling. Tier 2 has a premium, and it is holding. Tier 3 has only believers. But the believers happen to be the winners of the last 27 years of economic growth: globe spanning technology companies whose market capitalization rivals the GDP of the richest nation on Earth.

So what will you pay for AI?

For Tier 1, the bare minimum that clears the quality threshold.

For Tier 2, up to the value of not losing.

For Tier 3, perhaps a share of a future that does not yet exist.

The token is the same. The vig is not.

I work with a small number of companies each quarter on exactly this problem — which of your workflows are production, which are contests, which are options, and what each should cost you. Institutional Plan subscribers ($8K/yr) get a quarterly hour with me; for deeper engagements, email 8teapi@gmail.com.